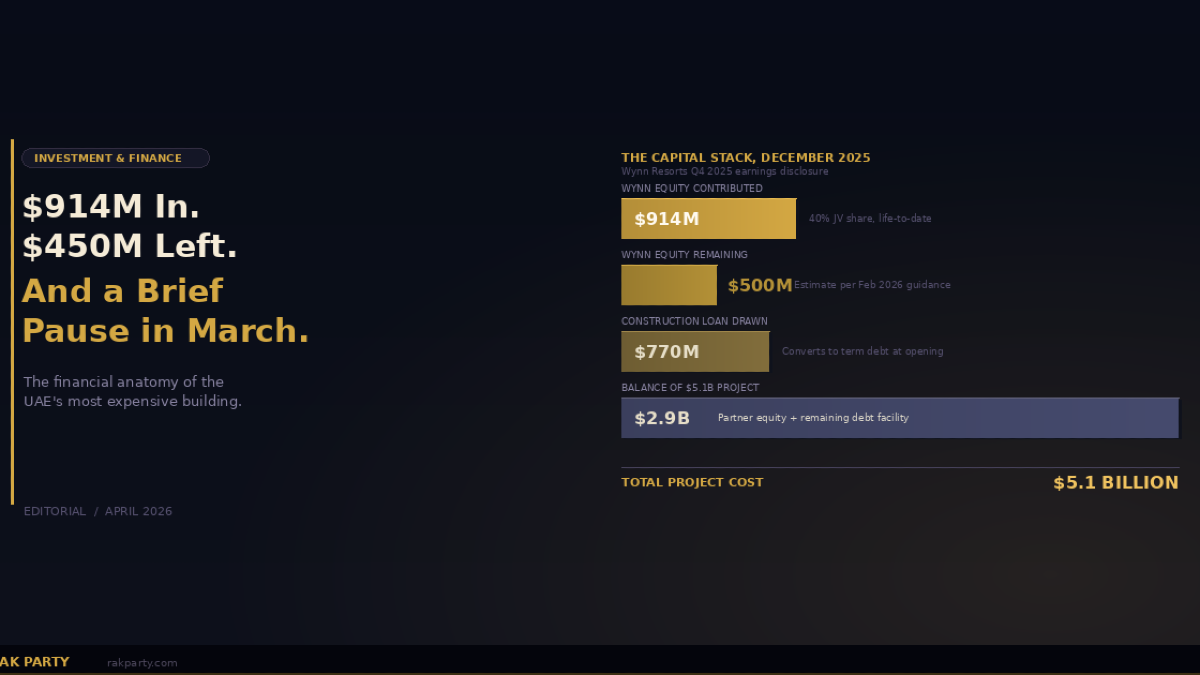

On February 12, 2026, at 4:30 pm Eastern time, Julie Cameron-Doe delivered her penultimate earnings presentation before retirement. Cameron-Doe had served as Chief Financial Officer of Wynn Resorts since April 2022, and the financial architecture of Wynn Al Marjan Island was effectively her deal. On the Q4 2025 earnings call, she read out four numbers that explained how a $5.1 billion project gets built. Wynn's equity contribution to the 40%-owned joint venture in the fourth quarter: $79.2 million. Total equity to date: $914.2 million. Remaining equity estimated: $450 million to $550 million. Construction loan drawn so far: $769.6 million.

Four numbers, one project, and a capital stack that almost nobody outside Wynn's investor relations team was reading closely. A month later, on March 11, 2026, Wynn Resorts issued a different press release. Construction on Al Marjan had resumed after "a brief pause" related to the broader regional security environment, the company said. Barry Lewis at ALEC Holdings, the lead contractor, confirmed that milestone timelines remained intact. The facade was at 79%. The low-rise buildings were at 99% structural completion. All 1,530 guest rooms had reached full structural completion. The pause happened. The pause ended. The money kept flowing.

This piece is about the financial architecture behind the UAE's most expensive building. Who owns what. How much Wynn has actually spent. What the construction loan looks like. What the brief pause in March actually meant. Why the outgoing CFO structured the deal the way she did. And why the $5.1 billion headline figure obscures the more interesting number: Wynn Resorts' equity exposure is materially smaller than most people assume, which is exactly why the board could approve the project at a scale that single-operator economics would never justify.

At a glance:Project cost: $5.1 billion. Wynn Resorts JV stake: 40% (partners: Marjan LLC and RAK Hospitality Holding). Wynn equity contributed to date (Dec 31, 2025): $914.2 million. Remaining Wynn equity required: $450-$550 million. Construction loan drawn: $769.6 million. Q4 2025 equity contribution: $79.2 million. 2026 expected equity contribution: $375-$400 million. 2027 expected: $75-$100 million. Opening: Spring 2027 (Q1 confirmed by Wynn in February 2026 earnings). Non-USD revenue target post-opening: over 55% of portfolio.

The $5.1 Billion Headline and What It Obscures

The figure that appears in every article about Wynn Al Marjan Island is $5.1 billion. It is the project's total development cost, covering land, design, construction, fit-out, pre-opening expenses, and the initial operating capital. Press releases cite it. Analysts reference it. Luxury travel publications repeat it. What almost none of them explain is that Wynn Resorts does not own the $5.1 billion asset. It owns 40% of a joint venture that owns the $5.1 billion asset. The broader resort picture (1,530 rooms, 22 restaurants, a 224,000 sq ft main casino floor, 420 metres of private beach) is what the capital is buying.

The joint venture partners are Wynn Resorts, Limited (the NASDAQ-listed operator and brand owner), Marjan LLC (the master developer of Al Marjan Island, wholly owned by the Government of Ras Al Khaimah), and RAK Hospitality Holding (the emirate's hospitality investment arm). Wynn holds 40%. The two Ras Al Khaimah partners together hold 60%. This is not the typical integrated-resort financing structure. At Marina Bay Sands in Singapore, Las Vegas Sands Corp owns the asset outright. At the Venetian Macao, the parent company bears the full equity risk. At Wynn Palace, Wynn owns the majority of Wynn Macau Limited, which in turn owns the property.

The Wynn Al Marjan Island structure is different. Wynn brings the brand, the operational expertise, the design team under Todd-Avery Lenahan at Wynn Design & Development, and a minority equity contribution. The two emirate-affiliated partners bring land, local government relationships, political alignment, and the majority of the equity. Wynn manages the property under a long-term contract. The economics of the arrangement are attractive for Wynn because its financial exposure is capped at 40% of the equity requirement while it captures management fees across the full revenue base of a project expected to generate $5-$8 billion in gaming revenue annually.

The Equity Schedule: $914 Million Down, $450-$550 Million to Go

As of December 31, 2025, Wynn Resorts had contributed $914.2 million in life-to-date equity to the Al Marjan joint venture. This figure is audited and disclosed in the Q4 2025 earnings release on February 12, 2026. The contribution pattern over recent quarters has accelerated as construction moved from structural concrete to interior fit-out, which is typical for integrated-resort development timelines. In Q3 2025, life-to-date contributions stood at $835 million. In Q4 2025, Wynn added $79.2 million, bringing the total to $914.2 million.

Cameron-Doe, speaking on the February 12 earnings call, guided investors to a remaining equity contribution estimate of approximately $450 million to $550 million across the remaining project timeline, which includes both Wynn Al Marjan Island and Wynn's share of the newly launched Janu Al Marjan Island joint venture. Management has separately indicated that approximately $375-$400 million of the remaining contributions will fall in calendar year 2026, with a further $75-$100 million expected in 2027. The back-loaded pattern reflects the interior fit-out and pre-opening activity that consumes capital most heavily in the final 12-18 months before opening.

Add the life-to-date $914.2 million to the projected remaining $450-$550 million and Wynn's total equity commitment to Al Marjan (combined with the Janu JV) resolves to approximately $1.37-$1.47 billion. On a $5.1 billion project cost base, that represents 27% to 29% of the total outlay, not the 40% implied by the JV ownership percentage. The difference is the construction loan. At the project level, the JV itself is 40%/60% equity between Wynn and the emirate-affiliated partners, but that equity is only part of the capital structure. The rest is debt.

The Construction Loan: $769.6 Million Drawn and Counting

Wynn Al Marjan Island is financed through a hybrid structure: equity from the joint venture partners and a dedicated construction loan that funds the project during the build phase. As of December 31, 2025, the construction loan had been drawn to $769.6 million, up from approximately $685 million at the end of Q3 2025. The loan will ultimately cover the remainder of the project cost not funded by equity contributions, and it converts to a term loan at or near opening in spring 2027.

The structural logic is standard for large hospitality development. Equity funds the early-stage expenses (design, site preparation, structural works) that carry the highest execution risk. Construction debt funds the later-stage expenses (interior fit-out, furniture-fixtures-equipment, pre-opening) once the project has demonstrated execution capability. The loan is secured against the project itself, with the JV partners guaranteeing their respective shares. At opening, the revenue stream services the debt directly from operating cash flow. Most integrated resorts, including the Venetian Macao and Marina Bay Sands in their original development phases, used comparable structures.

What distinguishes the Wynn Al Marjan Island loan from comparable transactions is the political context. The loan was arranged with regional and international lenders in an environment where UAE sovereign credit quality is exceptionally strong (both Abu Dhabi and the UAE federation hold AA ratings from S&P and Fitch) and where the Government of Ras Al Khaimah effectively stands behind the Marjan LLC equity contribution through RAK Hospitality Holding. The credit structure benefits from that sovereign backdrop even though Wynn itself carries the operator obligations.

The Original InsightThe $5.1 billion headline figure obscures the more interesting number: Wynn Resorts' equity exposure to Al Marjan is approximately $1.37-$1.47 billion, or roughly 27-29% of the project's total outlay, not 40%. This is a different financial animal than Marina Bay Sands or the Venetian Macao, where the operating company bears the full equity burden. Wynn's financial risk is materially smaller than the headline implies, which is exactly why the board could approve a project at a scale that single-operator economics would never justify. The minority-JV structure is the reason Wynn Al Marjan Island exists as a $5.1 billion project and not a $3 billion one.

March 11, 2026: What the Brief Pause Actually Meant

On March 11, 2026, Wynn Resorts issued an official statement on Wynn Al Marjan Island that most consumer publications missed entirely. Construction had resumed following a brief pause, the company said. The pause was related to the broader regional security environment (specifically, the ongoing US-Israel-Iran tensions that had intensified through early 2026) and steps had been taken to ensure the safety and security of all employees working on site. The company expressed confidence in the UAE's defense posture and in the federation's ability to maintain stability through the period of heightened risk.

The pause itself was short enough that Wynn's timeline guidance did not move. The Q1 2027 opening target was reconfirmed. The facade panels remained at 79% completion (a figure disclosed at the December 15, 2025 topping-out ceremony and still current through the March 11 update). All 1,530 guest accommodations remained at full structural completion. Interior fit-out remained active across 1,504 rooms. The Wynn Bridge, the 548-metre dedicated roadway connecting the resort to the E311 and E611 highways, remained at 48% complete with nine of ten bridge column pile caps in place. 18,000 construction jobs remained active.

The pause matters financially because it was the first visible test of the project's risk management under active regional tension. Wynn's statement was calibrated to reassure investors and partners without minimising the underlying security consideration. The company maintained communication with both the US government and the Ras Al Khaimah government through the pause, and the resumption was announced publicly within days rather than weeks. For a $5.1 billion asset under construction in a region where geopolitical risk is a permanent feature of the planning environment, the March 11 sequence (pause, safety verification, resumption, public disclosure) was approximately the ideal outcome. The project absorbed the shock and moved on.

The CFO Handover: Cameron-Doe, Fullalove, and What It Signals

Also announced on the February 12 earnings call: Julie Cameron-Doe will retire as Chief Financial Officer in mid-2026 and Craig Jeffrey Fullalove will succeed her. Cameron-Doe, who joined Wynn Resorts in April 2022, played a central role in securing the financing for Wynn Al Marjan Island, including the construction loan structure and the equity contribution schedule that governs the project through opening. She will remain with the company as a consultant and as a Non-Executive Director of Wynn Macau Limited, which maintains continuity on the Macau operations that contribute the largest share of Wynn's consolidated revenue.

The succession matters for Al Marjan because the remaining $450-$550 million in equity contributions, the conversion of the construction loan to term debt at opening, and the Q1 2027 commercial launch all fall within Fullalove's expected tenure. The structure Cameron-Doe put in place is locked. What Fullalove will manage is the execution of that structure through opening and the subsequent integration of Al Marjan's revenue into Wynn's consolidated financials. Wynn has framed the opening as a "free cash flow inflexion" for the company, using Craig Billings's exact language from the February 12 call. The CFO transition is timed so that Fullalove owns the inflexion.

Separately, on December 4, 2025, Wynn Resorts hosted an invitation-only Analyst & Investor UAE Market Tour at Wynn Al Marjan Island. Craig Billings and members of the global and Al Marjan management teams presented expected financial performance to institutional investors and sell-side analysts. The presentation was not webcast and the slide deck was posted briefly at 9:00 am Gulf Standard Time on the Wynn Resorts investor relations website. The tour itself is worth noting because it was the first time Wynn formalised the Al Marjan investment story for institutional audiences on the ground in Ras Al Khaimah. The analyst community walked the site, met the on-property management team, and received the pre-opening financial framework directly from Billings.

The 55% Non-USD Revenue Target: Why Al Marjan Is Strategic, Not Speculative

On the February 12 earnings call, Craig Billings framed the Wynn Al Marjan Island investment within a broader portfolio-level strategic position. "More broadly, we're moving toward a portfolio where we expect over 55% of our revenues will be generated in non-US dollar-denominated markets," he told investors, "from assets we developed and operate, each meticulously designed around the most valuable consumers in these markets." The statement deserves more attention than it received. Wynn is explicitly declaring that the majority of its future revenue will come from outside the United States.

The context matters. Wynn's FY2025 operating revenue was $7.14 billion, roughly flat against 2024's $7.13 billion. Las Vegas and Encore Boston Harbor together generate approximately $3.6 billion of that total. Wynn Palace and Wynn Macau generate approximately $3.4 billion. The split is close to 50/50 between USD-denominated and Macau pataca / Hong Kong dollar denominated. Al Marjan, when it opens, will add a third major revenue pool denominated in UAE dirham (pegged to the US dollar, so technically USD-denominated for accounting purposes but operationally dependent on non-US visitor flows). The 55%+ non-USD target assumes that Al Marjan's guest mix will skew heavily toward international visitors from Europe, Asia, the CIS region, and the Middle East, not from the United States.

Billings was explicit about the geopolitical logic. The world is becoming more multipolar, he said, and wealth creation is increasingly concentrated in three hubs: the United States, China, and the Middle East. Wynn's portfolio, with Las Vegas, Boston, Macau, and now Al Marjan, maps onto those three wealth hubs directly. The Al Marjan opening is the move that completes the geographic triangulation. It is also the move that reduces Wynn's dependence on any single macroeconomic cycle. If the US enters recession, Macau and the UAE continue operating. If China's gaming market softens, the US and UAE compensate. The diversification argument is the strategic case for spending $1.4 billion of Wynn equity on a minority JV position in a project 8,000 miles from the operator's headquarters.

What $1.47 Billion of Wynn Equity Actually Buys

For Wynn Resorts, the total equity commitment of approximately $1.37-$1.47 billion across Al Marjan and Janu delivers several assets. First, a 40% stake in the cash flows of a resort that analysts project will generate $5-$8 billion in gaming revenue annually, comparable to the Las Vegas Strip's $6 billion. Even at the low end of that range, Wynn's 40% share would be $2 billion in annual property-level gaming revenue, against an equity exposure of under $1.5 billion. The cash-on-cash return potential, assuming reasonable property-level EBITDA margins, is the strongest in any single development Wynn has undertaken.

Second, Wynn receives management fees on the full revenue base of the property. These fees are typically structured as a base fee (a percentage of total revenue) plus an incentive fee (a percentage of EBITDA or operating profit) and they flow to Wynn regardless of equity ownership. On a $5-$8 billion revenue base, management fees alone represent a material income stream for Wynn that is not duplicated in the equity returns.

Third, Wynn acquires the first-mover position in a regulated UAE gaming market with a 15-year license, no public plans from the federal government to issue additional licenses in the immediate future, and a pipeline of luxury hospitality development that positions Al Marjan Island as the center of Gulf casino tourism. The GCGRA regulatory framework grants Wynn effective operational monopoly through the initial license term. Competing operators would need to build from scratch in a market where the UAE's first casino already serves the established customer base, the established tourist flows, and the established regional high-roller network.

Fourth, Wynn gains a platform asset that supports the second resort already in planning on 155 acres adjacent to the current project, the Janu Al Marjan Island joint venture that will open in late 2028 under Aman Group's sister brand, and the 101-berth superyacht marina at the heart of the existing development. All three build on the infrastructure, the regulatory relationships, the brand recognition, and the operational team that $1.47 billion of upfront investment has already produced. The incremental cost of the second phase is materially smaller than the initial investment because the platform is in place.

How the Financial Structure Fits the Broader Strategy

The minority-JV structure at Al Marjan is a template that Wynn has indicated it may use for future international expansion. On the December 4 analyst tour and in subsequent earnings calls, Billings has described Al Marjan as both a standalone investment and a proof of concept for Wynn's ability to develop and operate integrated resorts in partnership with sovereign or sovereign-adjacent equity partners in emerging gaming markets. The structure solves the capital intensity problem that has historically constrained integrated-resort development in new jurisdictions. A single operator cannot easily commit $5 billion of its own equity to a project in an unfamiliar market. Two or three partners together can, and the returns still work.

This also explains Wynn's stated restraint on other potential projects. The company has a significant land bank in Las Vegas (analysts estimate value of $1 billion or more) and has been under pressure from some investors to flex that land bank into a new Strip development. Billings has consistently declined, citing the difficulty of creating market-share-taking economics when Las Vegas visitation is not growing. The capital discipline that keeps Wynn from overbuilding in Las Vegas is the same capital discipline that makes the minority-JV structure attractive for Al Marjan. Wynn is allocating capital where it earns the highest risk-adjusted return, and in the current environment that is the UAE.

The 1.35 million overnight visitors Ras Al Khaimah welcomed in 2025 and the emirate's 3.5 million target by 2030 are the demand-side forecast that supports the entire capital stack. If RAK hits the visitor target, the resort absorbs enough demand to service the debt, return capital to the JV partners, and generate the $5-$8 billion gaming revenue range Wynn's investor materials project. If RAK misses the target, the project still works because the construction loan is manageable against the 40% equity cushion, but the equity returns compress. The visitor growth story and the financial structure are the same story told in different currencies. The broader Al Marjan Island property market has already started pricing in the same demand curve.

Frequently Asked Questions

How much does Wynn Al Marjan Island cost?

$5.1 billion in total project cost, covering land, design, construction, fit-out, pre-opening expenses, and initial operating capital. The figure has been consistent across all Wynn Resorts press materials since early 2023.

Who owns Wynn Al Marjan Island?

It is owned by a joint venture structured as follows: Wynn Resorts, Limited holds 40%. Marjan LLC (wholly owned by the Government of Ras Al Khaimah) and RAK Hospitality Holding together hold 60%. Wynn operates the property under a long-term management agreement.

How much equity has Wynn contributed so far?

$914.2 million in life-to-date equity contributions as of December 31, 2025, per Wynn Resorts' Q4 2025 earnings release on February 12, 2026. Wynn added $79.2 million in Q4 2025 alone.

How much more does Wynn need to contribute?

Approximately $450-$550 million in remaining equity across 2026 and 2027, combined with contributions to the newly launched Janu Al Marjan Island joint venture. Most of the remaining contribution (approximately $375-$400 million) is expected in 2026, with $75-$100 million in 2027.

What is the construction loan drawn amount?

$769.6 million as of December 31, 2025. The construction loan funds the portion of the project not covered by equity contributions from the JV partners. It will convert to a term loan at or near opening in spring 2027.

When will Wynn Al Marjan Island open?

Spring 2027, specifically Q1 2027 per Wynn Resorts' Q4 2025 earnings guidance. Abdulla Al Abdouli, Group CEO of Marjan, confirmed March 2027 in a September 2025 Khaleej Times interview. The timeline was reconfirmed after the brief construction pause in March 2026.

What was the March 2026 construction pause?

On March 11, 2026, Wynn Resorts announced that construction had resumed following a brief pause related to the broader regional security environment. The pause was short enough that the Q1 2027 opening target remained intact. Facade at 79%, low-rise buildings at 99% structural completion, 1,530 rooms at full structural completion.

Who is the current CFO of Wynn Resorts?

Julie Cameron-Doe has served as CFO since April 2022 and will retire in mid-2026. Craig Jeffrey Fullalove will succeed her. Cameron-Doe will remain with Wynn as a consultant and as a Non-Executive Director of Wynn Macau Limited.

What are analysts projecting for gaming revenue at Wynn Al Marjan Island?

$5-$8 billion annually, per CEO Craig Billings on CNBC's Jim Cramer show in March 2025. For comparison, the Las Vegas Strip generates approximately $6 billion in annual gaming revenue across all operators combined.

How does the financial structure compare to Marina Bay Sands or the Venetian Macao?

Different. Marina Bay Sands is owned 100% by Las Vegas Sands Corp. The Venetian Macao is owned through Sands China (majority-owned by LVS). Wynn Al Marjan Island is 40%/60% between Wynn Resorts and emirate-affiliated partners. Wynn's equity exposure is materially smaller than the $5.1 billion headline implies, approximately $1.37-$1.47 billion, or 27-29% of total project cost.

What is the 55% non-USD revenue target?

On the February 12, 2026 earnings call, Craig Billings stated that Wynn is moving toward a portfolio where over 55% of revenues will be generated in non-US dollar-denominated markets. Al Marjan is the move that completes the geographic triangulation between the US, China (Macau), and the Middle East.

What was the December 4, 2025 analyst tour?

Wynn Resorts hosted an invitation-only Analyst & Investor UAE Market Tour at Wynn Al Marjan Island on December 4, 2025. Craig Billings and the management team presented expected financial performance to institutional investors and sell-side analysts on the ground in Ras Al Khaimah. The event was not webcast.

On February 12, 2026, Julie Cameron-Doe read out four numbers on an earnings call that most people did not attend. A month later, Wynn Resorts confirmed that construction had paused and then resumed. The numbers kept growing. $914.2 million contributed. $769.6 million drawn on the construction loan. $450-$550 million still to contribute. 40% of a $5.1 billion project, which is really 27-29% of the total outlay once you work through the capital stack. In spring 2027, the building opens. The construction loan converts to term debt. The management fees start flowing. Wynn's 55% non-USD revenue target moves from projection to measurable reality. The UAE's most expensive building becomes the UAE's most expensive operating property. Cameron-Doe will be consulting by then. Fullalove will be running the numbers. The capital stack Cameron-Doe designed will either work or it won't, and the answer will show up in Wynn's 2027 earnings releases. On current evidence, it will work.